In London’s West End, pedestrianized streets see a 30% increase in retail turnover compared to their car-clogged neighbors. You are not looking at a ‘lifestyle’ choice when you see people walking; you are looking at an efficient transaction engine. The data is consistent across global markets. Your walkability property value is not a subjective feeling or a preference for a specific demographic. It is a mathematical expression of accessibility and transaction density. When you increase the number of people who can reach a front door without a car, you increase the potential for revenue. This is the economics of proximity. It turns a physical asset into a high-yield financial instrument.

Many developers treat walkability as a ‘nice-to-have’ feature, placing it in the same category as a rooftop gym or a marble lobby. They are wrong. A marble lobby does not generate capital. Proximity to a network of walkable destinations does. Consequently, the market price of a property reflects this accessibility long before the architect draws a single line. Therefore, you must stop viewing walkability as a design choice and start viewing it as a risk-mitigation strategy.

TL;DR The Executive Summary +

- The perception of walkability as a 'lifestyle' luxury ignores its role as a primary driver of real estate yield and asset resilience.

- Research shows a 10-point Walk Score increase correlates with a 1% to 9% rise in commercial property value.

- We analyze cities as transaction engines where reducing the friction of distance directly increases the velocity of money.

- Prioritizing walkable density results in 10-20x higher tax revenue per acre and significantly higher retail turnover.

Why walkability property value is a mathematical certainty

The evidence is undeniable. Gary Pivo and Jeffrey Fisher analyzed over 4,000 commercial properties in the United States Pivo, G., & Fisher, J. D., 2011 — Real Estate Economics. They found that a 10-point increase in Walk Score leads to a 1% to 9% increase in property value depending on the asset class. This ‘Walkability Premium’ applies to office, retail, and apartment buildings. The reason is simple: humans seek efficiency. A city that forces you to spend 40 minutes in a metal box to buy a loaf of bread is an inefficient city. It wastes time, and time is the one resource your tenants cannot manufacture.

This leads to a fundamental truth about urban performance. A walkable environment reduces the ‘friction of distance’. When friction is low, the velocity of money increases. You see more transactions per hour, more spontaneous interactions, and higher occupancy rates. This is why walkability is a financial instrument. It creates a low-friction environment for capital to circulate. If you want to understand the deeper evidence behind these numbers, look at how we analyze Walkability Is Not a Lifestyle Choice. It’s a Financial Instrument..

The municipal debt trap of car-centric design

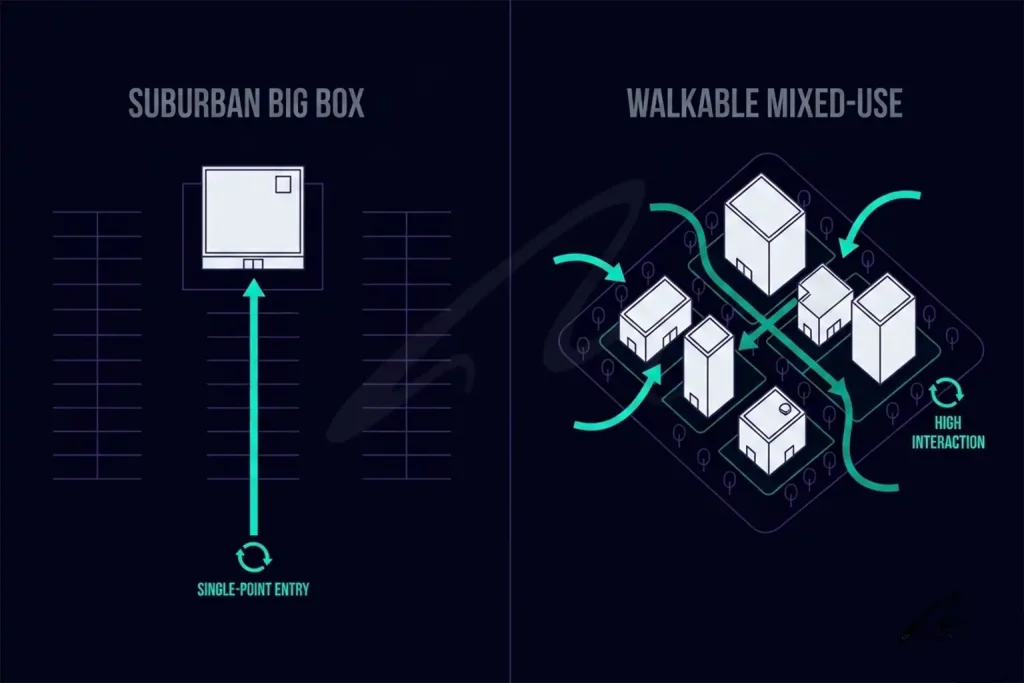

Furthermore, the fiscal health of the city depends on this metric. Look at the tax yield per acre. A typical suburban big-box store requires massive infrastructure—roads, sewers, power lines—to serve a single building surrounded by asphalt. The tax revenue per acre is abysmal. Contrast this with a traditional, walkable four-story mixed-use building. The walkable building produces ten to twenty times more tax revenue per acre for the city. Consequently, the car-centric model is a municipal debt trap. It creates liabilities that the tax base cannot support. The walkable model creates a surplus.

If you are an investor, this means your ‘green’ building in a car-dependent suburb is a liability. You might have the best solar panels, but if your tenants must drive to reach you, you have failed. You are betting against the physics of the city. You are ignoring the 5 Metrics Every Architect Should Put in Their Fee Proposal that actually drive long-term value. One of those metrics is the catchment area’s walkability. Retailers already know this. They don’t look at the ‘beauty’ of a street. They look at footfall and dwell time. A car-centric strip mall has high footfall but zero dwell time outside the store. A walkable street has both. This creates accidental commerce. You cannot design accidental commerce in a parking lot. You can only facilitate it through permeable urban fabric.

The psychology of dwell time and turnover

The sidewalk is not a transit corridor. It is a revenue-generating platform. Every meter of sidewalk width in a high-density area correlates with increased retail turnover. This isn’t a guess. It is the result of how humans perceive space. We do not spend money when we feel unsafe or rushed. A narrow sidewalk next to high-speed traffic creates a high-cortisol environment. Consequently, people leave as quickly as possible. A wide, shaded sidewalk with active frontages creates a low-cortisol environment. People slow down. This ‘slowing down’ is what converts a passerby into a customer.

The result is a more resilient asset. During economic downturns, walkable neighborhoods hold their value better than suburban ones. They offer flexibility. A walkable storefront can transition from a bakery to a gallery to a tech office. A suburban big-box store is hard to repurpose. This flexibility is a form of embedded insurance. It protects the owner from market shifts. Therefore, the next time a planning committee asks about the ‘cost’ of wider sidewalks, change the conversation. Do not talk about ‘quality of life’. Talk about yield per square meter. Talk about the internal rate of return. You are not asking for a favor; you are presenting a way to make the project more profitable. The The Carbon Argument Is Losing. The Human Argument Is Winning. because the human argument is tied directly to the wallet.

Walkability is the most reliable predictor of urban economic health. It is the bridge between the physical world of architecture and the abstract world of finance. Stop designing for cars. Start designing for the velocity of transactions. Your balance sheet will thank you.

You Might Be Wondering

Honest answers to real objections